Active Watchlist

SRTA

Strata Critical Medical, Inc.

90score

Focused post-Blade medical infrastructure platform for organ-transplant logistics, surgical recovery, organ placement, NRP/perfusion, staffing, and equipment. The market may still price SRTA as legacy passenger/eVTOL-adjacent aviation or low-margin logistics, while the upside case is a one-call mission-critical transplant infrastructure consolidator with network-density advantages, clinical-service optionality, improving cash conversion, and bolt-on M&A evidence.

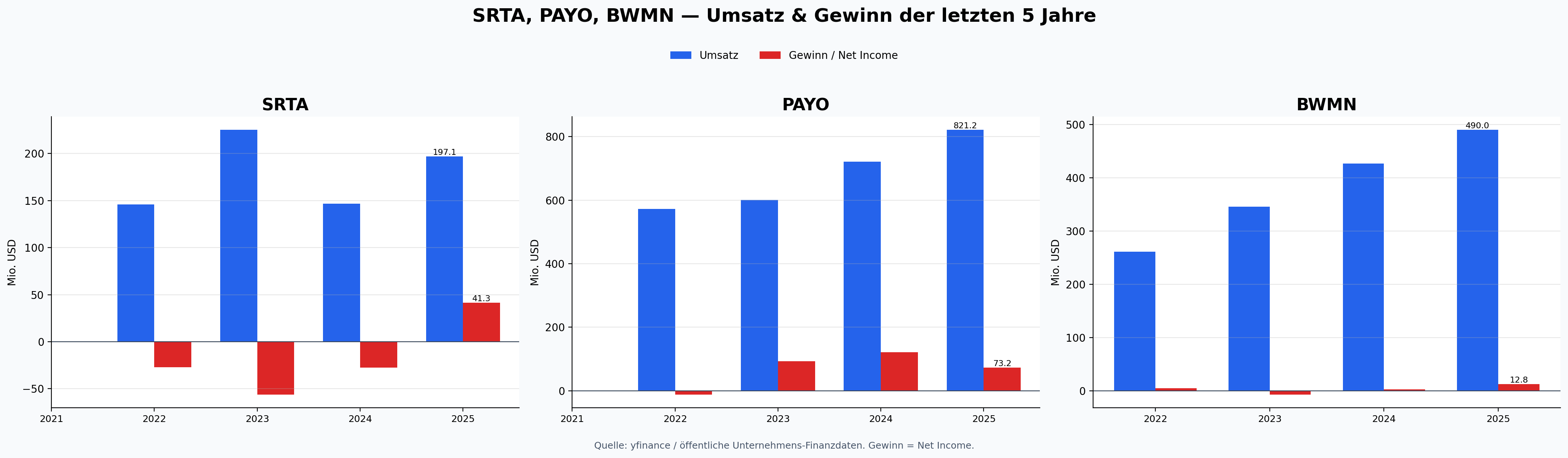

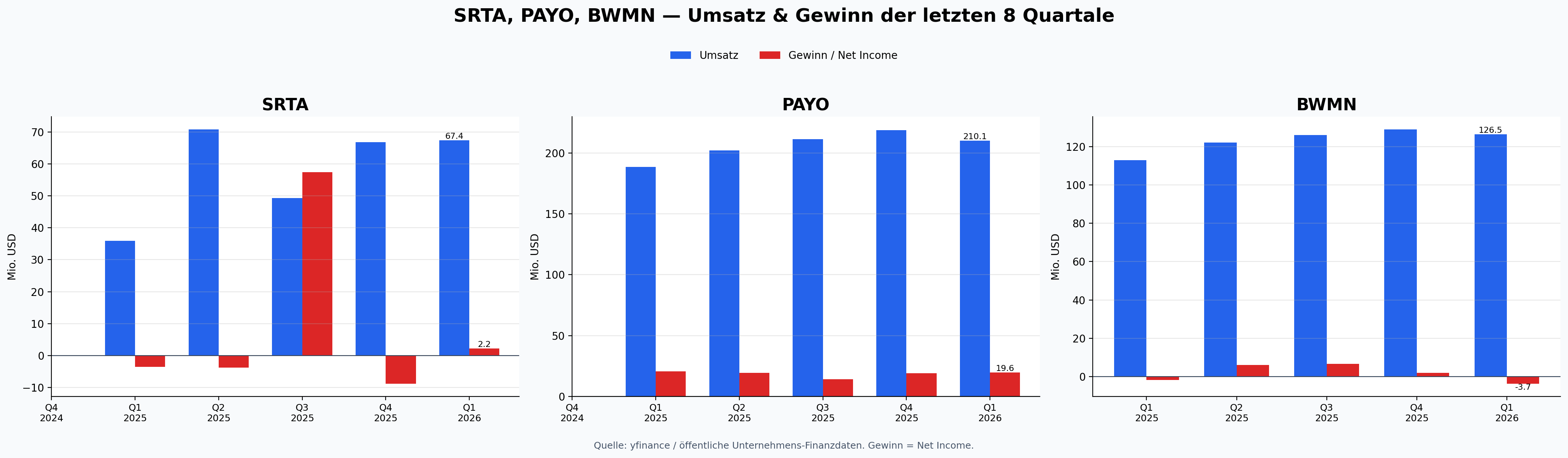

Approx. $509M market cap using yfinance last price $5.88 on 2026-06-21 and 86.5M shares outstanding from the Q1 2026 10-Q; Q1 2026 revenue $67.4M (+87.4% YoY), logistics revenue +32.4% organically, net income from continuing operations $2.4M, adjusted EBITDA $6.4M; FY2026 guidance $260M-$275M revenue, $29M-$33M adjusted EBITDA, $15M-$22M FCF before aircraft/engine acquisitions.

scale economies logistics clinical staffing compliancenetwork density effects opo transplant center coverageswitching costs workflows protocols trustprocess power dispatch recovery perfusion qualitycornered resource specialized staff logistics transplant trustcounter positioning one call medical platform vs fragmented vendors

Kill / sell rules

- Remove if FY2026 guidance is materially cut without a one-off explanation.

- Remove if two consecutive quarters show weak organic logistics growth plus no clinical margin improvement.

- Remove if free cash flow before aircraft/engine acquisitions fails to convert despite adjusted EBITDA.

- Remove if management resumes unfocused aviation/passenger optionality.

- Remove if acquisitions become large/dilutive/unintegrated or safety/regulatory failures damage trust.

Active Watchlist

PAYO

Payoneer Global Inc.

84score

Global SMB cross-border commerce infrastructure mispriced as a commodity/rate-sensitive fintech. Payoneer combines regulated local rails, marketplace relationships, multi-currency accounts, AP/AR, working capital, and payout workflows across 7,000+ corridors and nearly 2M active customers. If core volume reaccelerates and margins scale, it has a plausible 5-10 year path to multi-billion revenue and $15B+ equity value.

Approx. $1.8B equity value using Yahoo chart price around $4.96 and ~360M share count estimate; Q1 2026 revenue $261.6M, operating income $30.0M, net income $19.6M.

switching costsscale economiesbrandpartial network effectscornered resource regulatory local railsprocess power risk compliance localization

Kill / sell rules

- Remove if two consecutive quarters show deteriorating active customers plus sub-10% core revenue growth.

- Remove if compliance/fraud losses materially impair trust.

- Remove if management uses cash for dilutive or unfocused M&A.

- Remove if gross/transaction economics structurally compress.

- Remove if thesis depends mainly on interest income rather than durable payments volume.

Active Watchlist

BWMN

Bowman Consulting Group Ltd.

82score

Founder-led national infrastructure engineering/services consolidator in a fragmented AEC market. The market may price Bowman as a cyclical consultant, while the upside case is a Strata-like hidden workflow platform: local mission-critical relationships plus national scale, geospatial/automation tooling, public infrastructure tailwinds, and a bolt-on acquisition flywheel.

Approx. $0.55B equity value using Yahoo chart price around $33.32 and Q1 2026 weighted average shares of ~16.45M; Q1 2026 gross contract revenue $126.5M, net loss $3.7M, adjusted EBITDA $16.8M.

scale economiesswitching costs client project historyprocess power acquisition integration geospatial QAbrand emerginglimited network effects cross office referralscounter positioning mid sized local national model

Kill / sell rules

- Remove if leverage rises above a conservative service-business range without credible deleveraging path.

- Remove if two or more quarters show revenue growth driven mostly by acquisitions while margins/backlog deteriorate.

- Remove if cash conversion remains poor for a full year.

- Remove if Gary Bowman materially reduces involvement without proven succession.

- Remove if acquisitions become larger and strategically unfocused.

Watchlist High Risk Convex

SDGR

Schrödinger, Inc.

7.4score

Computational chemistry / molecular-design software platform with drug-discovery optionality; could become mission-critical R&D infrastructure if AI-enabled molecular simulation adoption broadens.

5–10x plausible but high risk if software/platform revenue scales to $500–700M+, margins become software-like, and pipeline/milestone economics add upside from a sub-$1B market cap.

987807936

Kill / sell rules

- software revenue stalls for multiple quarters

- annual cash burn accelerates without commercial traction

- cash runway below roughly two years

- management shifts too far toward self-funded biotech risk

- gross margin/platform retention deteriorates

Key risks

- weak or lumpy revenue growth

- high operating burn

- internal pipeline consuming too much capital

- AI drug-discovery hype compression

- software retention/gross margin deterioration

Active Watchlist

XMTR

Xometry, Inc.

86score

AI-native custom-manufacturing marketplace that could become the procurement and execution infrastructure layer for fragmented machine shops and enterprise buyers. If Xometry’s buyer/supplier network, instant quoting, enterprise workflows, and Siemens Xcelerator partnership create a durable digital thread from design to delivered parts, it has a plausible 5-10 year path to multi-billion revenue and a 5-10x equity outcome.

Approx. $5.0B market cap / $5.1B enterprise value at yfinance price ~$95.29; TTM revenue ~$740.8M; cash ~$224.0M; debt ~$339.8M. Q1 2026 revenue $205.1M (+36% YoY), marketplace revenue $191.3M (+40% YoY), net loss $5.3M, adjusted EBITDA $10.5M.

network effects two sided marketplacescale economies pricing sourcing dataswitching costs enterprise procurement workflowscounter positioning asset light marketplace vs brokers and capex heavy shopsprocess power ai quoting supplier matching fulfillmentbrand enterprise manufacturing

Kill / sell rules

- Remove if active buyer growth falls below low-teens for two consecutive quarters while revenue growth slows materially.

- Remove if marketplace gross margin reverses structurally or supplier quality/on-time delivery problems damage trust.

- Remove if adjusted EBITDA turns negative again without a clear high-ROI investment reason.

- Remove if Siemens/Xcelerator integration fails to produce observable enterprise demand or strategic validation over 12-24 months.

- Remove if dilution/debt-funded expansion outruns gross-profit growth or cash conversion.

Active Watchlist

VHI.TO / VHIBF

VitalHub Corp.

87score

Healthcare workflow software consolidator: EHR, patient flow, care coordination, clinical workflow, workforce and patient-engagement tools. The market may view VitalHub as a small Canadian healthcare-software roll-up, while the asymmetric thesis is a mission-critical healthcare operating layer with sticky regulated workflows, high gross margins, organic ARR growth, cross-sell, and disciplined tuck-in M&A across fragmented health systems.

Approx. CAD $446M market cap from StockAnalysis TSX:VHI snapshot on 2026-06-18/19; FY2024 revenue $68.6M, ARR $71.1M (+59% YoY), organic ARR growth 15%, gross margin 81%, adjusted EBITDA $17.8M / 26% margin.

switching costs healthcare workflow embeddingscale economies R&D compliance sales implementationprocess power vertical software M&A integrationbrand healthcare workflow reputationcornered resource domain specific clinical workflows

Kill / sell rules

- Remove if organic ARR growth falls below high-single-digits for two consecutive years without M&A offset.

- Remove if acquisition pace causes margin compression, integration failures, or debt/dilution that outruns ARR growth.

- Remove if gross margin or adjusted EBITDA margin deteriorates structurally.

- Remove if healthcare systems do not expand usage/cross-sell across modules.

Active Watchlist

LMB

Limbach Holdings, Inc.

85score

Mission-critical building-systems infrastructure platform for mechanical, electrical, plumbing, and controls systems. The market may treat LMB as a cyclical contractor; the better thesis is a higher-quality owner-direct service platform for healthcare, industrial, data-center, life-sciences, education, and other uptime-critical facilities, with recurring relationships, margin mix shift, local density and bolt-on consolidation optionality.

Approx. $0.95B-$1.0B market cap from June 2026 market-data references; FY2025 revenue $646.8M (+24.7% YoY), Owner Direct Relationships revenue $485.7M (+40.6%) and ~75% of total revenue, net income $39.1M, FY2026 guidance $730M-$760M revenue and $90M-$94M adjusted EBITDA with free cash flow expected around 75% of adjusted EBITDA.

switching costs facility relationships system history uptime trustprocess power owner direct MEPC execution and service modelscale economies procurement labor recruiting branch densitycounter positioning owner direct vs low margin general contractor workbrand mission critical building systems

Kill / sell rules

- Remove if ODR mix falls materially or GCR work regains dominance.

- Remove if adjusted EBITDA growth does not convert to free cash flow over a full year.

- Remove if acquisitions become large/unfocused or integration damages margins.

- Remove if backlog/organic growth weakens in core mission-critical verticals for multiple quarters.

Active Watchlist

IIIV

i3 Verticals, Inc.

84score

Focused GovTech/public-sector workflow software platform after divesting merchant services and healthcare RCM. The market may still view IIIV as a messy payments roll-up with slow headline growth; the asymmetric thesis is a mission-critical, regulated public-sector operating layer across courts/public safety, public administration/ERP, transportation, utilities, and education, with 5,000+ contracted customers, recurring revenue, embedded payments, sticky implementations, and a long fragmented modernization/M&A runway.

Approx. $416M public Class A market-cap snapshot from yfinance at $21.29 on 2026-06-28; economic equity value is higher if Class B/non-controlling units are included. Fiscal Q2 2026 revenue from continuing operations was $57.5M (+6.2% YoY), ARR was $183.5M (+11.6% YoY), net income from continuing operations was $2.2M, and adjusted EBITDA was $16.6M / 28.8% margin; FY2026 guidance after Q2 was narrowed/lowered, so reacceleration must be proven.

switching costs public sector implementations data workflows paymentsscale economies R&D security compliance support procurementprocess power vertical GovTech M&A and domain implementationcornered resource public sector domain relationships and procurement knowledgebrand trusted public sector software partnercounter positioning focused mid market GovTech suite vs point vendors and legacy systems

Kill / sell rules

- Remove if ARR growth falls below high-single-digits for two consecutive quarters without a clear transition explanation.

- Remove if SaaS/recurring revenue strength fails to translate into consolidated revenue reacceleration by FY2027.

- Remove if adjusted EBITDA margin drops below the low-20s due to integration problems or product sprawl.

- Remove if acquisition spending becomes dilutive/unfocused or debt outruns ARR and free-cash-flow growth.

- Remove if public-sector customer retention, implementation quality, or cybersecurity/compliance trust deteriorates.

Active Watchlist

EVI

EVI Industries, Inc.

83score

Small public buy-and-build platform for commercial and industrial laundry infrastructure: equipment distribution, facility design/planning, installation, parts, maintenance, repair, boiler/mechanical systems, water heating, power generation, and water-reuse systems. The market may price EVI as a low-margin equipment distributor, while the asymmetric thesis is a one-call mission-critical infrastructure and service platform for fragmented laundry/boiler workflows serving healthcare, hospitality, government, industrial, correctional, education, food/beverage, cruise and retail customers.

Approx. $207M market cap / $276M enterprise value from yfinance at $16.09 on 2026-07-05. Fiscal 2025 revenue was $389.8M (+10.3% YoY) and net income was $7.5M; latest reported quarter ended 2026-03-31 revenue was $101.1M and net income was $0.75M. Balance sheet leverage rose after acquisitions: yfinance snapshot showed about $73.0M debt and $4.3M cash, so margin/cash conversion must improve for the 10x case to work.

process power buy and build M&A integration and local operator networkscale economies supplier terms inventory parts technician densityswitching costs facility design installation service history and uptime trustcounter positioning decentralized local service platform vs single market distributorsbrand emerging national laundry infrastructure partnercornered resource technician network supplier relationships and installed base knowledge

Kill / sell rules

- Remove if organic growth remains low-single-digit while acquisition debt rises or share dilution accelerates.

- Remove if gross margin or operating margin does not improve after recent acquisitions are integrated.

- Remove if free cash flow fails to cover working-capital needs and acquisition-related debt service over a full year.

- Remove if management deviates from disciplined small tuck-ins into large/unrelated deals.

- Remove if supplier/customer relationships weaken, technician availability constrains service, or project delays turn backlog into poor cash conversion.

Active Watchlist

RDVT

Red Violet, Inc.

86score

Identity-intelligence and risk/compliance data platform hiding in a small-cap wrapper. Red Violet's idiCORE/IDI and FOREWARN products sit inside fraud prevention, identity verification/authentication, due diligence, legislative compliance, debt recovery, law-enforcement/government, real-estate safety, collections and corporate-security workflows. The market may price RDVT as an expensive niche data vendor; the asymmetric thesis is a high-gross-margin, cloud-native identity graph and workflow rail where more data, more customers, API/batch integrations and specialized compliance use cases compound into a mission-critical fraud/risk infrastructure platform.

Approx. $954M market cap / $913M enterprise value from yfinance at $67.59 on 2026-07-12. Q1 2026 revenue was $25.8M (+17% YoY), gross margin was 75%, adjusted gross margin 85%, net income $4.4M, adjusted EBITDA $10.7M / 41% margin, operating cash flow $6.6M, and cash/equivalents $43.5M. FY2025 revenue was $90.3M (+20%), gross profit $65.1M, net income $13.2M, and yfinance financials show FY2025 EBITDA about $23.8M.

scale economies data ingestion cloud AI compliance salesswitching costs API batch workflows investigative training and compliance recordsprocess power identity graph matching data quality and risk scoringcornered resource longitudinal identity graph and permissible use compliance knowhowbrand trust in fraud risk real estate safety and investigationsnetwork data effects more queries customers feedback and data sources improve utility

Kill / sell rules

- Remove if revenue growth falls below low-teens for two consecutive quarters without a clear macro/customer-budget explanation.

- Remove if adjusted EBITDA margin falls below 30% while revenue growth is also decelerating, indicating loss of operating leverage.

- Remove if data-privacy, permissible-use, FCRA/GLBA/DPPA, law-enforcement or real-estate safety trust issues materially impair customer adoption.

- Remove if IDI billable-customer growth or FOREWARN user/association growth stalls for multiple quarters.

- Remove if valuation remains rich while the company fails to expand beyond current identity/fraud/real-estate verticals into broader compliance and risk workflows.

Active Watchlist

TRAK

ReposiTrak, Inc.

84score

Food traceability and supplier-compliance rails hiding inside a tiny profitable SaaS/network company. ReposiTrak operates a hub-and-spoke B2B platform where retailers/wholesalers pull suppliers into compliance, traceability and supply-chain workflows. The market may punish flat near-term revenue and delayed FSMA 204 enforcement, while the upside case is that industry-led traceability requirements, recall readiness, supplier records, Touchless Traceability patents/processes and a growing food-supply network turn TRAK into a mission-critical compliance/traceability operating layer for fragmented grocery, wholesale, foodservice and supplier ecosystems.

Approx. $160M market cap / $134M enterprise value from yfinance at $8.81 on 2026-07-19; shares outstanding 18.17M per FY2026 Q3 10-Q. TTM revenue about $23.5M, gross margin about 85%, EBITDA margin about 35%, profit margin about 31%, cash about $26.4M and essentially no bank debt. FY2026 Q3 revenue was $5.88M (-1% YoY), operating income $2.25M (+24% YoY), net income $1.99M, and nine-month FY2026 revenue was $17.71M (+5%) with operating income $5.96M (+28%).

network effects hub spoke retailers wholesalers suppliers traceability recordsswitching costs supplier onboarding KDE CTE compliance workflows audit historyprocess power touchless traceability 500 point validation data ingestionscale economies SaaS compliance network sales support data validationcornered resource food traceability network supplier records and retail relationshipscounter positioning no hardware label or scanning disruption vs heavy ERP traceability projects

Kill / sell rules

- Remove if traceability/onboarding activity does not convert into double-digit recurring revenue growth by FY2027/FY2028.

- Remove if FDA FSMA 204 enforcement delay to July 2028 causes customers to pause adoption and industry-led requirements do not fill the gap.

- Remove if gross margin falls below 75% or operating margin falls below 20% while revenue is flat or declining.

- Remove if hubs stop pulling suppliers into the network, supplier-record growth stalls, or the hub-and-spoke network effect weakens.

- Remove if larger ERP/supply-chain vendors or retailers replicate Touchless Traceability with lower switching cost before TRAK reaches broader network density.

Key risks

- Revenue growth is currently only low-single-digit/flat despite high margins.

- FDA FSMA 204 enforcement has been pushed toward July 2028, which may slow urgency.

- Tiny revenue base and customer/hub concentration can make growth lumpy.

- Large ERP, EDI, supply-chain, distributor or retailer-owned systems could compete.

- Valuation can compress if TRAK remains a niche compliance tool rather than a broad network rail.

Active Watchlist

TCS.TO / TCYSF

Tecsys Inc.

85score

Mission-critical supply-chain execution software for healthcare and complex distribution hiding in a small Canadian public company. The market may view Tecsys as a slow, niche WMS/vendor-services company with modest GAAP profit; the asymmetric thesis is a sticky operating layer for hospital supply chains, pharmacies/health systems and complex distributors where inventory visibility, compliance, replenishment, warehouse execution and integration reliability matter. If Elite SaaS migration, healthcare penetration, AI-driven TecsysIQ workflows and Gartner-recognized WMS credibility compound, TCS can become a scarce healthcare/distribution supply-chain infrastructure platform.

Approx. CAD $477.6M market cap from StockAnalysis TSX:TCS snapshot as of 2026-07-24; yfinance showed 14.34M shares outstanding and recent TSX close around CAD $31.94-$33.09. FY2026 revenue was CAD $193.1M (+9.5% YoY), SaaS revenue CAD $80.4M (+20%), SaaS ARR CAD $86.8M (+13% / +15% constant currency), net profit CAD $4.0M, and adjusted EBITDA CAD $20.0M / 10% margin.

switching costs healthcare distribution supply chain workflows integrations trainingprocess power supply chain execution WMS healthcare domain and implementation knowhowscale economies SaaS R&D AI security support and implementationbrand trust mission critical healthcare and distribution supply chainscornered resource domain specific healthcare supply chain data workflows and customer relationshipscounter positioning vertical healthcare distribution execution vs horizontal ERP and generic WMS

Kill / sell rules

- Remove if Elite SaaS revenue growth falls below low-teens for two consecutive years without clear migration timing explanation.

- Remove if SaaS ARR growth stays below 10% while professional-services/hardware mix remains necessary to drive headline revenue.

- Remove if adjusted EBITDA margin fails to expand toward mid-teens as SaaS mix rises by FY2028.

- Remove if healthcare win rates/backlog weaken materially or government/health-system budget delays become structural.

- Remove if larger ERP/WMS vendors neutralize Tecsys' vertical differentiation or implementation quality/customer trust deteriorates.

Key risks

- Total revenue growth is only high-single-digit, so the 10x case depends on SaaS acceleration and margin expansion, not current consolidated growth.

- Healthcare and government-related buying cycles can delay implementations and make quarterly growth lumpy.

- Large ERP/WMS vendors, healthcare IT incumbents and supply-chain suites can compete aggressively.

- Professional-services implementation capacity may constrain growth or pressure margins.

- Small-cap Canada liquidity and valuation risk can amplify drawdowns if growth disappoints.